Global Thermal Management Technologies Market Statistics: USD 24.8 Billion Value by 2032

Thermal Management Technologies Industry

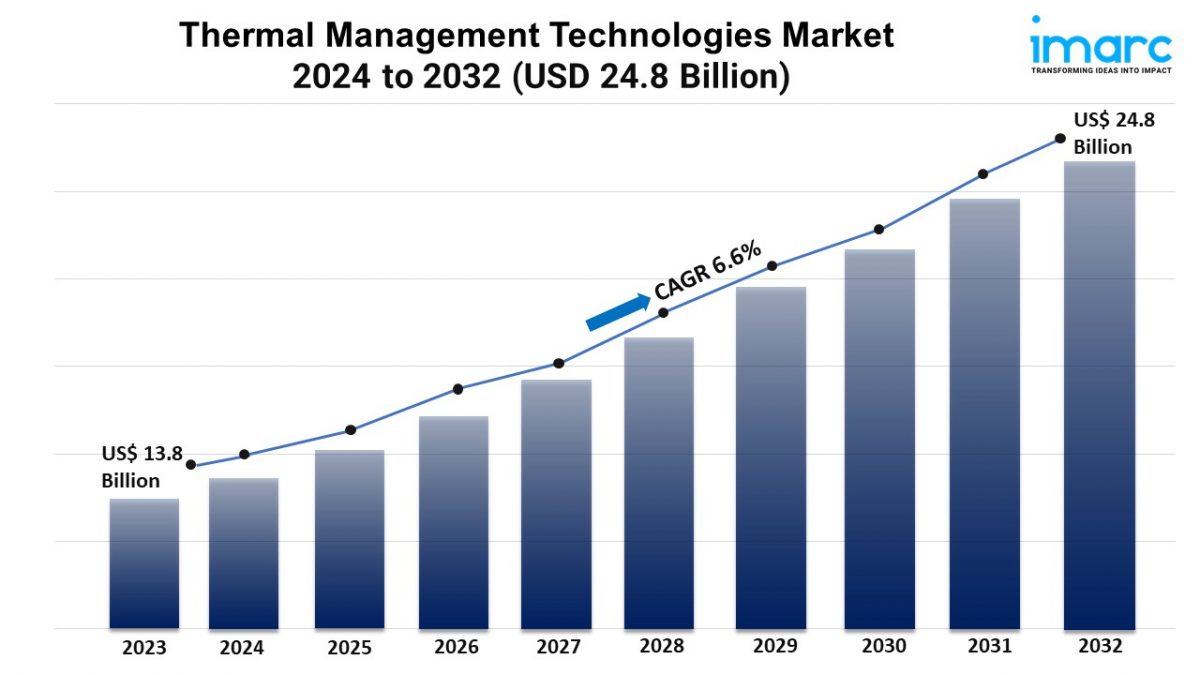

Summary:

- The global thermal management technologies market size reached USD 13.8 Billion in 2023.

- The market is expected to reach USD 24.8 Billion by 2032, exhibiting a growth rate (CAGR) of 6.6% during 2024-2032.

- North America leads the market, accounting for the largest thermal management technologies market share.

- Hardware accounts for the majority of the market share in the product segment as it is designed to dissipate, control, and regulate heat.

- Computers hold the largest share in the thermal management technologies industry.

- The rising demand for electronic devices is a primary driver of the thermal management technologies market.

- Growth of the data center industry and technological advancements in electric vehicles (EVs) are reshaping the thermal management technologies market.

Industry Trends and Drivers:

- Growing Demand for Electronic Devices:

The growing adoption of personal electronic devices like smartphones, laptops, tablets, and wearables among the masses across the globe is catalyzing the demand for thermal management technologies. As these devices become more powerful and compact, the heat generated by their components increases, which can reduce performance and longevity. Manufacturers are prioritizing advanced cooling solutions to maintain device efficiency and user safety. Innovations, such as passive heat sinks, fans, and liquid cooling systems, are gaining traction to manage excess heat effectively. With consumers demanding devices that are both high-performance and durable, the integration of sophisticated thermal management systems is becoming essential. Furthermore, the trend toward miniaturization in electronics amplifies the need for efficient heat dissipation in tight spaces.

- Growth of the Data Center Industry:

Data centers play a critical role in modern computing, particularly with the rise of cloud services, artificial intelligence (AI), and big data analytics. These facilities house massive amounts of hardware, such as servers and networking equipment, which generate substantial heat during operation. Efficient thermal management solutions are essential for maintaining optimal temperatures, preventing equipment failures, and reducing energy costs. As data centers expand to handle growing internet traffic, their need for more advanced cooling systems, such as liquid immersion cooling and AI-driven airflow optimization, intensifies. In line with this, environmental concerns and regulations push data center operators to adopt sustainable and energy-efficient thermal technologies.

- Technological Advancements in Electric Vehicles (EVs):

The escalating demand for innovative thermal management solutions due to shift toward EVs is propelling the market growth. EV batteries, motors, and power electronics produce significant amounts of heat that must be controlled to ensure vehicle safety, performance, and longevity. Thermal management systems play a crucial role in preventing battery overheating, which can degrade battery life and efficiency. As EV manufacturers push the boundaries of vehicle performance and range, more advanced cooling technologies, such as phase-change materials, liquid cooling, and thermoelectric coolers, are being developed. The rapid expansion of the EV market, coupled with stricter regulations on emissions and energy efficiency, is supporting the market growth.

Request for a sample copy of this report: https://www.imarcgroup.com/thermal-management-technologies-market/requestsample

Thermal Management Technologies Market Report Segmentation:

Breakup By Product:

- Hardware

- Software

- Interface

- Substrates

Hardware accounts for the majority of shares as it is designed to dissipate, control, and regulate heat.

Breakup By Application:

- Computers

- Consumer Electronics

- Telecommunication

- Automotive

- Renewable Energy

- Others

Computers dominate the market on account of the rising focus on preventing overheating and maintaining product performance.

Breakup By Region:

- North America (United States, Canada)

- Asia Pacific (China, Japan, India, South Korea, Australia, Indonesia, Others)

- Europe (Germany, France, United Kingdom, Italy, Spain, Russia, Others)

- Latin America (Brazil, Mexico, Others)

- Middle East and Africa

North America enjoys the leading position owing to a large market for thermal management technologies driven by the presence of a robust technological ecosystem, including major tech companies, data centers, and automotive manufacturers.

Top Thermal Management Technologies Market Leaders:

The thermal management technologies market research report outlines a detailed analysis of the competitive landscape, offering in-depth profiles of major companies. Some of the key players in the market are:

- Advanced Cooling Technologies Inc.

- Autoneum Holding AG

- Gentherm Inc.

- Heatex Inc. (Madison Industries)

- Henkel AG & Co. KGaA

- Honeywell International Inc.

- Laird Thermal Systems Inc.

- Momentive Performance Materials Inc.

- Parker-Hannifin Corp.

- Thermal Management Technologies

If you require any specific information that is not covered currently within the scope of the report, we will provide the same as a part of the customization.

About Us:

IMARC Group is a global management consulting firm that helps the world’s most ambitious changemakers to create a lasting impact. The company provide a comprehensive suite of market entry and expansion services. IMARC offerings include thorough market assessment, feasibility studies, company incorporation assistance, factory setup support, regulatory approvals and licensing navigation, branding, marketing and sales strategies, competitive landscape and benchmarking analyses, pricing and cost research, and procurement research.

Contact Us:

IMARC Group

134 N 4th St. Brooklyn, NY 11249, USA

Email: sales@imarcgroup.com

Tel No:(D) +91 120 433 0800

United States: +1-631-791-1145 | United Kingdom: +44-753-713-2163