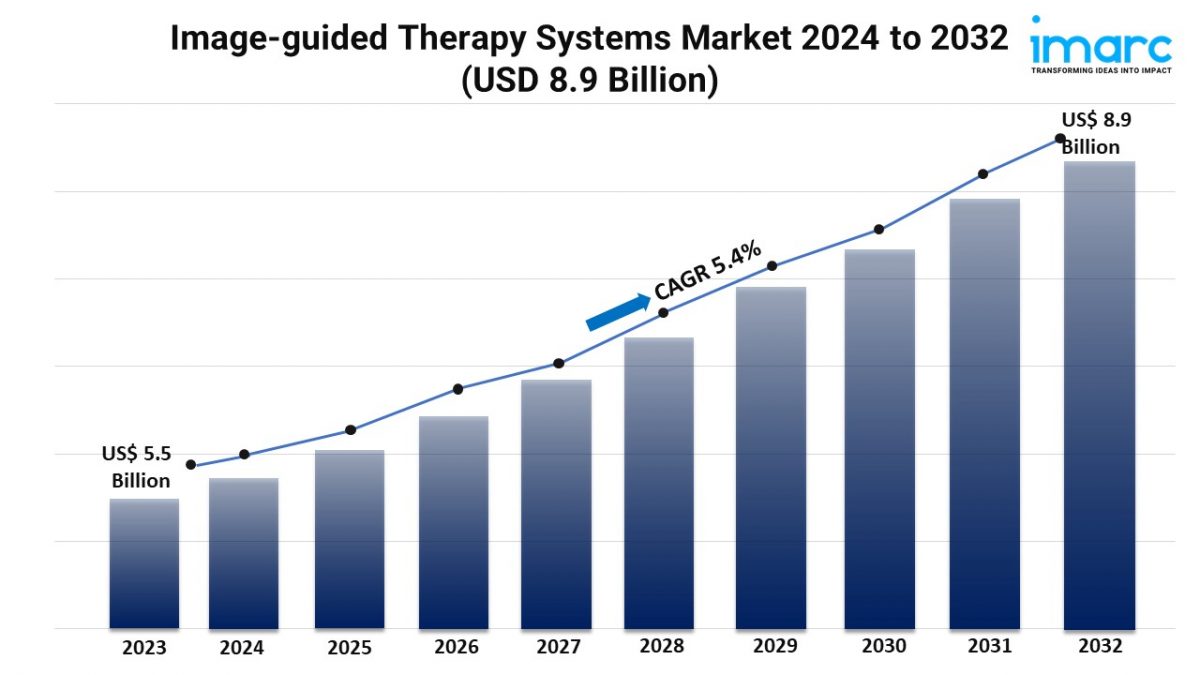

Global Thermal Management Technologies Industry: Key Statistics and Insights in 2024-2032

Summary:

- The global thermal management technologies market size reached USD 13.8 Billion in 2023.

- The market is expected to reach USD 24.8 Billion by 2032, exhibiting a growth rate (CAGR) of 6.6% during 2024-2032.

- North America leads the market, accounting for the largest thermal management technologies market share.

- Hardware accounts for the majority of the market share in the product segment due to its functionality and efficiency in dissipating heat in various electronic devices.

- Computers represent the leading application segment.

- The increasing need for electronic devices and smart systems is a primary driver of the thermal management technologies market.

- Technological advancements in electric vehicles (EVs) and renewable energy systems are reshaping the thermal management technologies market.

Industry Trends and Drivers:

- Growing Demand for Electronic Devices and Systems

The rapid proliferation of electronic devices, from smartphones and laptops to data centers and automotive electronics, is impelling the market growth. As these devices become more compact and powerful, they generate more heat, necessitating advanced thermal management solutions to ensure optimal performance and longevity. The rise of the internet of things (IoT) and 5G networks further drives this need, as numerous interconnected devices require efficient thermal regulation to function reliably. In data centers, high-performance computing and increased server densities lead to higher heat outputs, prompting the need for sophisticated cooling solutions. Moreover, the continuous evolution of electronic devices and systems is driving innovation in thermal management technologies, including advanced materials, heat sinks, heat pipes, and liquid cooling systems to effectively manage and dissipate heat.

- Advancements in Electric Vehicles (EVs) and Renewable Energy Systems

The transition towards electric vehicles (EVs) and renewable energy systems is propelling the market growth. EVs, in particular, rely heavily on effective thermal management to maintain battery performance, longevity, and safety. High-capacity batteries and power electronics in EVs generate significant heat, requiring advanced cooling systems to prevent overheating and ensure efficient operation. Moreover, renewable energy systems like solar panels and wind turbines need effective thermal management to optimize energy conversion rates and prolong equipment lifespan. In both cases, innovative thermal management solutions are essential to address the unique cooling requirements of these technologies. As the adoption of EVs and renewable energy systems is growing, the demand for advanced thermal management technologies is increasing.

- Increased Focus on Energy Efficiency and Sustainability

There is a heightened emphasis on energy efficiency and sustainability across industries, which is positively influencing the market. Companies are increasingly focused on reducing energy consumption and minimizing environmental impact, driving the need for more efficient thermal management solutions. Traditional cooling methods, such as air conditioning in data centers or industrial applications, are being supplemented or replaced by more energy-efficient alternatives like liquid cooling, advanced phase-change materials, and thermoelectric cooling systems. These technologies offer better heat dissipation with lower energy consumption, aligning with global sustainability goals. Additionally, government regulations and initiatives aimed at reducing carbon footprints are encouraging the adoption of eco-friendly thermal management solutions. As a result, the demand for innovative, energy-efficient thermal management technologies is rising.

Request for a sample copy of this report: https://www.imarcgroup.com/thermal-management-technologies-market/requestsample

Thermal Management Technologies Market Report Segmentation:

Breakup By Product:

- Hardware

- Software

- Interface

- Substrates

Hardware represents the largest segment due to the widespread adoption of directly managing and dissipating heat in various electronic devices and systems.

Breakup By Application:

- Computers

- Consumer Electronics

- Telecommunication

- Automotive

- Renewable Energy

- Others

Computers hold the biggest market share, as the demand for efficient thermal management solutions is critical to maintaining high-performance computing environments.

Breakup By Region:

- North America (United States, Canada)

- Asia Pacific (China, Japan, India, South Korea, Australia, Indonesia, Others)

- Europe (Germany, France, United Kingdom, Italy, Spain, Russia, Others)

- Latin America (Brazil, Mexico, Others)

- Middle East and Africa

North America dominates the market owing to its strong technological infrastructure, high concentration of data centers, and leading position in the development and adoption of advanced electronics and renewable energy systems.

Top Thermal Management Technologies Market Leaders:

The thermal management technologies market research report outlines a detailed analysis of the competitive landscape, offering in-depth profiles of major companies. Some of the key players in the market are:

- Advanced Cooling Technologies Inc.

- Autoneum Holding AG

- Gentherm Inc.

- Heatex Inc. (Madison Industries)

- Henkel AG & Co. KGaA

- Honeywell International Inc.

- Laird Thermal Systems Inc.

- Momentive Performance Materials Inc.

- Parker-Hannifin Corp.

- Thermal Management Technologies

If you require any specific information that is not covered currently within the scope of the report, we will provide the same as a part of the customization.

About Us:

IMARC Group is a global management consulting firm that helps the world’s most ambitious changemakers to create a lasting impact. The company provide a comprehensive suite of market entry and expansion services. IMARC offerings include thorough market assessment, feasibility studies, company incorporation assistance, factory setup support, regulatory approvals and licensing navigation, branding, marketing and sales strategies, competitive landscape and benchmarking analyses, pricing and cost research, and procurement research.

Contact Us:

IMARC Group

134 N 4th St. Brooklyn, NY 11249, USA

Email: sales@imarcgroup.com

Tel No:(D) +91 120 433 0800

United States: +1-631-791-1145 | United Kingdom: +44-753-713-2163