Global Biosensors Industry: Key Statistics and Insights in 2024-2032

Biosensors Industry

Summary:

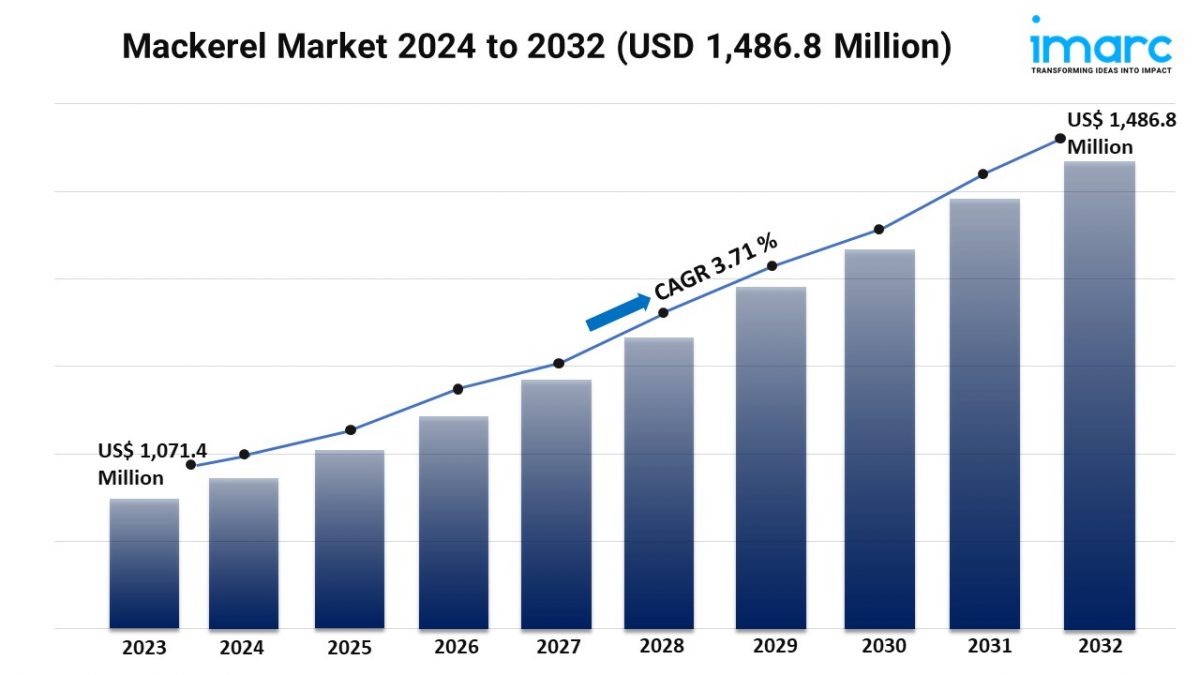

- The global biosensors market size reached USD 28.8 Billion in 2023.

- The market is expected to reach USD 55.4 Billion by 2032, exhibiting a growth rate (CAGR) of 7.3% during 2024-2032.

- North America leads the market, accounting for the largest biosensors market share.

- Non-wearable biosensors account for the majority of the market share in the product segment due to their widespread use in clinical diagnostics and laboratory settings.

- Electrochemical biosensors hold the largest share in the biosensors industry.

- Blood glucose testing represents the leading application segment.

- Point of care testing remains a dominant segment in the market, owing to the increasing need for rapid, accurate diagnostics in decentralized healthcare settings.

- The increase in the occurrence of chronic diseases is a primary driver of the biosensors market.

- Technological advancements in nanotechnology, microelectronics, and biotechnology are reshaping the biosensors market.

Biosensors Market Trends and Drivers:

- Increasing Prevalence of Chronic Diseases:

The rising incidence of chronic diseases, such as diabetes, cardiovascular disorders, and cancer, is impelling the growth of the market. Patients with chronic conditions require continuous monitoring of physiological parameters like glucose levels, heart rate, and other biomarkers. Biosensors offer a non-invasive, rapid, and reliable way to monitor these indicators, making them indispensable in healthcare. Moreover, glucose biosensors are revolutionizing diabetes management by allowing real-time blood sugar monitoring, enhancing patient autonomy, and improving treatment outcomes. As chronic diseases become more prevalent due to aging populations and lifestyle factors, the demand for biosensor technologies is rising. This trend is further strengthened by the push for personalized healthcare, where biosensors enable tailored treatment plans and early intervention.

- Technological Advancements and Miniaturization:

Ongoing advancements in nanotechnology, microelectronics, and biotechnology are crucial in expanding the capabilities and applications of biosensors. Miniaturization of biosensors allows for the development of portable, wearable, and even implantable devices, offering convenience and continuous health monitoring. Wearable biosensors, like fitness trackers, provide real-time data on various health metrics, such as heart rate and oxygen levels, contributing to both consumer health awareness and clinical care. These innovations not only enhance the precision and sensitivity of biosensors but also expand their usability in diverse settings, including home healthcare and remote monitoring. Furthermore, technological progress has led to lower manufacturing costs, making biosensors more accessible and widespread across different sectors such as food safety, environmental monitoring, and defense.

- Growing Demand for Point-of-Care Diagnostics:

Point-of-care (POC) diagnostics is another major factor driving the adoption of biosensors. With the growing emphasis on early diagnosis and personalized treatment, there is a shift toward decentralized healthcare solutions that can deliver quick, accurate results outside of traditional laboratory settings. Biosensors, with their ability to detect a wide range of biological markers, are integral to POC diagnostic tools, facilitating rapid decision-making in critical scenarios. This trend is particularly relevant in developing countries and remote areas where access to sophisticated healthcare infrastructure is limited. Additionally, the emergence of novel infectious diseases is driving the demand for biosensors in POC applications, particularly for rapid testing and disease surveillance.

Request for a sample copy of this report: https://www.imarcgroup.com/biosensors-market/requestsample

Biosensors Market Report Segmentation:

Breakup By Product:

- Wearable Biosensors

- Non-Wearable Biosensors

Non-wearable biosensors exhibit a clear dominance in the market due to their widespread use in clinical diagnostics and laboratory settings, offering high precision and reliability for various medical and research applications.

Breakup By Technology:

- Electrochemical Biosensors

- Optical Biosensors

- Piezoelectric Biosensors

- Thermal Biosensors

- Nanomechanical Biosensors

- Others

Electrochemical biosensors represent the largest segment because they offer high sensitivity, cost-effectiveness, and versatility, making them ideal for detecting a wide range of analytes in medical and environmental monitoring.

Breakup By Application:

- Blood Glucose Testing

- Cholesterol Testing

- Blood Gas Analysis

- Pregnancy Testing

- Drug Discovery

- Infectious Disease Testing

- Others

Blood glucose testing holds the biggest market share as diabetes management requires continuous and real-time monitoring, driving the demand for glucose biosensors globally.

Breakup By End Use:

- Point of Care Testing

- Home Healthcare Diagnostics

- Research Laboratories

- Security and Biodefense

- Others

Point of care testing accounts for the majority of the market share, driven by the increasing need for rapid, accurate diagnostics in decentralized healthcare settings, allowing for immediate decision-making.

Breakup By Region:

- North America (United States, Canada)

- Asia Pacific (China, Japan, India, South Korea, Australia, Indonesia, Others)

- Europe (Germany, France, United Kingdom, Italy, Spain, Russia, Others)

- Latin America (Brazil, Mexico, Others)

- Middle East and Africa

North America dominates the market attributed to advanced healthcare infrastructure, high adoption of innovative technologies, and a growing focus on personalized medicine and chronic disease management.

Top Biosensors Market Leaders:

The biosensors market research report outlines a detailed analysis of the competitive landscape, offering in-depth profiles of major companies. Some of the key players in the market are:

- Abbott Laboratories

- AgaMatrix Inc. (WaveForm Technologies Inc)

- DuPont de Nemours Inc.

- F. Hoffmann-La Roche AG

- General Electric Company

- LifeScan Inc. (Platinum Equity LLC)

- Medtronic PLC

- Nova Biomedical Corporation

- PHC Holdings Corporation

- Siemens AG

- Thermo Fisher Scientific Inc.

If you require any specific information that is not covered currently within the scope of the report, we will provide the same as a part of the customization.

About Us:

IMARC Group is a global management consulting firm that helps the world’s most ambitious changemakers to create a lasting impact. The company provide a comprehensive suite of market entry and expansion services. IMARC offerings include thorough market assessment, feasibility studies, company incorporation assistance, factory setup support, regulatory approvals and licensing navigation, branding, marketing and sales strategies, competitive landscape and benchmarking analyses, pricing and cost research, and procurement research.

Contact Us:

IMARC Group

134 N 4th St. Brooklyn, NY 11249, USA

Email: sales@imarcgroup.com

Tel No:(D) +91 120 433 0800

United States: +1-631-791-1145 | United Kingdom: +44-753-713-2163