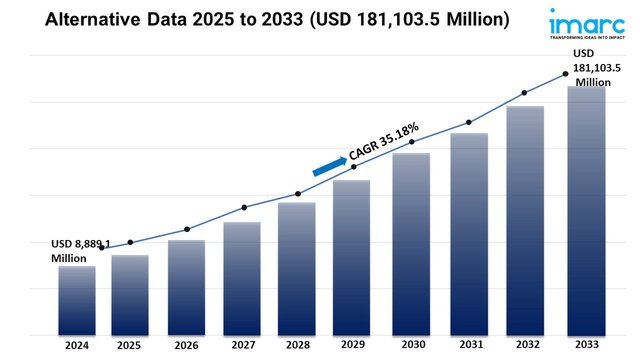

The thermal paper market is a dynamic and evolving sector, driven by the increasing demand for efficient, cost-effective printing solutions across industries like retail, logistics, healthcare, and gaming. Valued at USD 4.51 billion in 2024 , the global thermal paper market is projected to reach USD 6.78 billion by 2033 , growing at a compound annual growth rate (CAGR) of 4.40% during the forecast period (2025–2033), according to IMARC Group. This growth is fueled by technological advancements, the rise of e-commerce, and the need for sustainable alternatives, but it also faces challenges like regulatory restrictions and environmental concerns.

In this comprehensive blog post, we’ll dive into the thermal paper market, exploring its definition, key trends, regulatory landscape, growth drivers, challenges, and future opportunities. Whether you’re a business owner, industry professional, or simply curious about this niche market, this guide will provide valuable insights into the forces shaping its trajectory.

Overview of the Thermal Paper Market

The thermal paper market encompasses the production, distribution, and application of specialty paper coated with heat-sensitive chemicals that change color when exposed to heat. This unique property makes thermal paper an ideal choice for applications requiring quick, ink-free printing, such as receipts, labels, tickets, and tags. The market serves a wide range of industries, including retail, logistics, healthcare, food and beverage, and gaming, with point-of-sale (POS) systems being the largest application segment.

The market’s growth is driven by the increasing adoption of POS terminals, the expansion of e-commerce, and advancements in thermal printing technology. However, the industry is also navigating challenges such as environmental concerns over non-recyclable thermal paper and regulatory restrictions on chemical coatings like bisphenol-A (BPA). Despite these hurdles, the market is poised for steady growth, with opportunities in eco-friendly innovations and emerging applications.

What Is Thermal Paper?

Thermal paper, often referred to as an audit roll, is a specialty paper coated with a heat-sensitive layer that reacts to heat from a thermal printer to produce images, text, or barcodes. traditional printing methods that require ink or toner, thermal paper relies on a chemical reaction between heat-sensitive dyes and developers, such as BPA or bisphenol-S (BPS), to create high-quality prints. This makes it a cost-effective and efficient solution for applications where a permanent record is not required.

Thermal paper is used in various devices, including:

- Point-of-Sale (POS) Systems : For printing receipts in retail stores, restaurants, and gas stations.

- Labeling : For shipping labels, product tags, and barcode labels in logistics and e-commerce.

- Ticketing : For transportation tickets, parking tickets, and event tickets.

- Gaming and Lottery : For printing lottery tickets and gaming receipts.

- Healthcare : For medical labels, prescription tags, and patient wristbands.

There are two primary types of thermal printing technologies:

- Direct Thermal : The paper is coated with a heat-sensitive layer that darkens when heated by a thermal printhead. This method is widely used for receipts and shipping labels due to its simplicity and cost-effectiveness. In 2023, direct thermal held over 51% of the market share.

- Thermal Transfer : This method uses a ribbon to transfer ink onto the paper, offering more durable prints suitable for long-term applications like barcode labels. It is expected to grow at a CAGR of 4.8% through 2030.

Case Study: Thermal Paper in Retail

A major US retailer implemented 80mm direct thermal paper rolls across its 1,000+ stores for POS receipt printing. The switch to thermal paper reduced printing costs by 20% compared to traditional ink-based systems and improved checkout efficiency. The retailer also adopted BPA-free thermal paper to align with consumer demand for safer, eco-friendly products, enhancing its brand reputation.

Key Trends Shaping the Thermal Paper Market

The thermal paper market is evolving rapidly, driven by technological advancements, changing consumer preferences, and industry-specific demands. Below are the key trends influencing the market in 2025 and beyond:

1. Rise of E-Commerce and Logistics

The global e-commerce market, valued at USD 26.8 trillion in 2024, is projected to grow at a CAGR of 25.83% through 2033. This boom has increased the demand for thermal paper in shipping labels, packing slips, and invoices. Logistics companies rely on thermal paper for its smudge-proof and moisture-resistant properties, ensuring clear, durable prints for tracking and delivery purposes.

2. Adoption of Eco-Friendly Thermal Paper

Environmental concerns and regulatory restrictions on BPA have spurred the development of BPA-free and phenol-free thermal paper. Companies like Hansol Paper and Appvion have introduced sustainable products, such as Appvion’s EarthChem portfolio, which uses eco-friendly coatings. This trend aligns with consumer demand for recyclable and biodegradable materials.

3. Advancements in Thermal Printing Technology

Innovations in thermal printers, such as high-speed printing and improved durability, have enhanced the reliability of thermal paper. For example, top-coated thermal paper, which offers better resistance to environmental factors like heat and moisture, is gaining traction in logistics and healthcare. The top-coated segment is projected to grow at a CAGR of 10.5% through 2032.

4. Growth in Mobile POS Systems

The increasing use of mobile POS terminals in retail, hospitality, and transportation has boosted demand for compact thermal paper rolls, particularly 57mm widths. These portable printers are used for on-the-go billing, ticketing, and delivery receipts, driving the 57mm segment’s projected CAGR of 4.7% through 2030.

5. Expansion in Healthcare and Pharmaceutical Applications

Thermal paper is increasingly used in healthcare for printing RFID tags, prescription labels, and patient wristbands. Stringent labeling regulations in pharmaceuticals have further fueled demand for thermal transfer paper, which offers durable, high-quality prints for compliance and traceability.

Case Study: Thermal Paper in Healthcare

A leading hospital chain in Europe adopted thermal transfer paper for its RFID-based patient identification system. The durable labels ensured accurate tracking of patient records and medications, reducing errors by 15%. The hospital also switched to BPA-free thermal paper to comply with EU regulations, improving patient safety.

Regulatory Landscape

The thermal paper market operates under a complex regulatory framework, particularly concerning the use of chemical coatings like BPA and BPS. Governments and regulatory bodies worldwide are implementing stricter guidelines to address health and environmental concerns. Below are the key regulations impacting the market:

1. Restrictions on Bisphenol-A (BPA)

BPA, a common developer in thermal paper, has been linked to health issues such as endocrine disruption and reduced fertility. The European Union (EU) banned BPA in thermal paper effective January 2020, limiting its concentration to 0.02% by weight. The United States Environmental Protection Agency (EPA) has also introduced guidelines to phase out BPA, prompting manufacturers to adopt BPS or phenol-free alternatives.

2. Environmental Regulations

Thermal paper is challenging to recycle due to its chemical coatings, raising environmental concerns. Regulations in regions like the EU and North America encourage the use of recyclable and biodegradable materials. For example, the EU’s Circular Economy Action Plan emphasizes sustainable packaging, pushing manufacturers to develop eco-friendly thermal paper.

3. Food Safety Regulations

In the food and beverage industry, thermal paper used for labeling must comply with stringent safety standards to prevent chemical migration into food. The US Food and Drug Administration (FDA) and the EU’s Food Contact Materials Regulation (EC) No 1935/2004 set guidelines for safe materials, driving demand for BPA-free and food-safe thermal paper.

4. Regional Variations

Regulatory requirements vary by region. For instance, Asia-Pacific countries like China and Japan have less stringent BPA regulations, but increasing consumer awareness is pushing manufacturers to adopt safer alternatives. In contrast, North America and Europe have robust frameworks, influencing global market trends toward sustainability.

Case Study: Regulatory Compliance in Europe

A major thermal paper manufacturer in Germany faced challenges complying with the EU’s BPA ban. By investing in R&D, the company developed a phenol-free thermal paper that met regulatory standards and gained a competitive edge. The product’s success led to a 10% increase in market share in the EU.

Market Growth Drivers

The thermal paper market’s projected growth to USD 6.78 billion by 2033 is driven by several factors, including industry-specific demands and technological advancements. Below are the primary growth drivers:

1. Thriving E-Commerce Sector

The rapid expansion of e-commerce, particularly in Asia-Pacific and North America, has increased the need for thermal paper in logistics. Shipping labels and tracking tags, which account for a significant portion of thermal paper usage, are essential for efficient supply chain management.

2. Increasing POS Terminal Adoption

The POS segment, which held 67% of the market share in 2023, continues to drive growth. The modernization of POS systems with features like wireless connectivity and touchscreens has broadened their application in retail, hospitality, and healthcare.

3. Technological Advancements

Innovations in thermal printing, such as high-speed printers and durable top-coated paper, have improved print quality and reliability. These advancements make thermal paper a preferred choice over traditional printing methods, boosting market demand.

4. Regional Growth

North America, with a 33.09% market share in 2021, is expected to grow at a CAGR of 4.87% through 2032, driven by retail and manufacturing expansion. The Asia-Pacific region, projected to grow at a CAGR of 11.3%, is fueled by industrial activity in China and Japan.

5. Different Industry Applications

Thermal paper’s versatility supports its use in healthcare, pharmaceuticals, food and beverage, and gaming. For example, the food and beverage sector relies on thermal paper for hygienic, high-quality labels that comply with regulatory standards.

Challenges in the Thermal Paper Market

Despite its growth potential, the thermal paper market faces several challenges that could hinder its progress. Addressing these issues is critical for sustained market expansion.

1. Environmental Concerns

Traditional thermal paper is difficult to recycle due to its chemical coatings, contributing to waste. The shift toward digital receipts, as announced by e-commerce giants in February 2024, further threatens demand in retail applications.

2. Regulatory Restrictions

Strict regulations on BPA and BPS limit the use of traditional thermal paper, increasing production costs for manufacturers developing safer alternatives. Compliance with varying regional standards also poses logistical challenges.

3. Competition from Digital Alternatives

The rise of digital receipts and e-ticketing, particularly in retail and transportation, reduces the need for thermal paper. While some industries prefer physical records for returns or warranties, digital solutions are gaining traction in regions with advanced infrastructure.

4. Supply Chain Disruptions

The COVID-19 pandemic highlighted vulnerabilities in global supply chains, temporarily disrupting thermal paper production and distribution. Raw material shortages and logistics delays continue to pose risks.

5. Health Concerns

Consumer awareness of BPA’s health risks has led to demand for safer alternatives, but BPS and other substitutes are also under scrutiny. Manufacturers must invest in R&D to develop non-toxic coatings, increasing costs.

Case Study: Overcoming Environmental Challenges

A Japanese thermal paper manufacturer faced declining sales due to environmental concerns. By partnering with a recycling firm, the company developed a recyclable thermal paper that reduced waste by 30%. The initiative not only addressed environmental challenges but also attracted eco-conscious clients, boosting sales by 12%.

Future Opportunities

The thermal paper market is ripe with opportunities, particularly in sustainability, innovation, and emerging markets. Below are the key areas of potential growth:

1. Eco-Friendly Innovations

The development of BPA-free, phenol-free, and recyclable thermal paper presents significant opportunities. Companies like Lecta, which launched BPA-free Termax thermal grades in February 2024, are setting the stage for sustainable growth.

2. Expansion in Emerging Markets

Asia-Pacific, particularly China and India, offers untapped potential due to rapid industrialization and retail growth. Investments in local production facilities can help manufacturers capitalize on this demand.

3. Integration with Smart Technologies

The integration of thermal paper with RFID and IoT technologies in healthcare and logistics can enhance traceability and efficiency. For example, RFID-enabled thermal labels improve inventory management in warehouses.

4. Customized Solutions

Offering tailored thermal paper products, such as top-coated paper for high-durability applications or specialty widths for niche markets, can attract new customers. Customization is particularly valuable in healthcare and pharmaceuticals.

5. Partnerships and Collaborations

Collaborations between manufacturers and technology providers can drive innovation. For instance, partnerships with POS system developers can lead to optimized thermal paper solutions for modern retail environments.

Case Study: Innovation in Logistics

A global logistics firm partnered with a thermal paper manufacturer to develop top-coated, RFID-enabled thermal labels for its supply chain. The labels improved tracking accuracy by 25% and reduced operational costs, demonstrating the potential of smart thermal paper solutions.

Conclusion

The thermal paper market is at a pivotal moment, balancing growth opportunities with environmental and regulatory challenges. the industry is driven by the rise of e-commerce, POS adoption, and technological advancements. However, challenges like BPA regulations, recycling difficulties, and digital alternatives require proactive solutions.

The future of the thermal paper market lies in sustainability and innovation. By embracing eco-friendly coatings, expanding into emerging markets, and integrating smart technologies, manufacturers can stay ahead of the curve. As industries like retail, logistics, and healthcare continue to rely on thermal paper for efficient printing, the market’s resilience and adaptability will ensure its relevance in the years to come.

Whether you’re a stakeholder in the thermal paper industry or simply interested in its evolution, staying informed about these trends and opportunities is key to navigating this dynamic market. For more insights, explore industry reports from trusted sources like IMARC Group or connect with market research experts to stay ahead of the curve.