Global Sugar Industry: Key Statistics and Insights in 2024-2032

Summary:

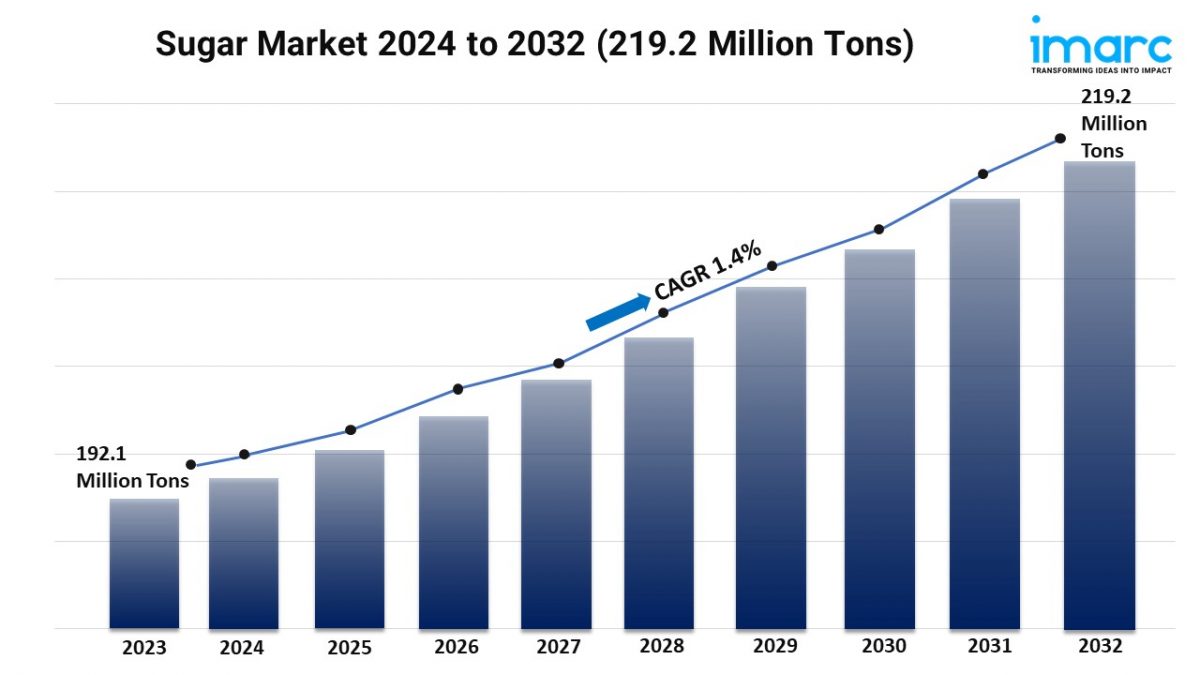

- The global sugar market size reached USD 192.1 Million in 2023.

- The market is expected to reach USD 219.2 Million by 2032, exhibiting a growth rate (CAGR) of1.4% during 2024-2032.

- Brazil leads the market, accounting for the largest sugar market share.

- White sugar accounts for the majority of the market share in the product type segment due to its long shelf life and versatility in culinary applications.

- Granulated sugar holds the largest share in the sugar industry.

- Food and beverages remain a dominant segment in the market owing to the growing global demand for convenience and processed food products.

- Sugarcane represents the leading source segment.

- The rising demand from the food and beverage (F&B) industry is a primary driver of the sugar market.

- Technological advancements and ethanol production are reshaping the sugar market.

Industry Trends and Drivers:

- Ethanol production:

Ethanol is primarily produced from sugarcane in countries like Brazil. The demand for ethanol as a biofuel pushes farmers and producers to allocate more sugarcane for ethanol production rather than sugar refining. In Brazil, sugar mills have the flexibility to switch between producing sugar or ethanol, depending on which market offers better profitability. When ethanol prices are high, a larger proportion of sugarcane is diverted to ethanol production, reducing sugar supply and potentially driving up global sugar prices. Several countries, including the US, Brazil, and those in the European Union, have set mandates requiring the blending of ethanol with gasoline to reduce carbon emissions.

- Demand from food and beverage (F&B) industry:

Sugar is a fundamental ingredient in a variety of processed food products, including baked goods, confectionery, cereals, and snacks. As consumer demand for convenient, ready-to-eat foods grows, especially in urbanized areas, the F&B industry’s need for sugar increases. In developing economies, as disposable incomes rise, there’s a shift towards higher consumption of packaged and processed foods, further boosting sugar demand. Sugar is a core component in soft drinks, energy drinks, flavored milk, juices, and other sweetened beverages. The global beverage industry, particularly in markets like the US, China, and India, continues to see high demand for these products. As the demand for sugary beverages grows, it drives up sugar consumption, especially in regions where beverage consumption is increasing rapidly due to growing middle-class populations and lifestyle changes.

- Technological advancements:

The adoption of precision agriculture techniques, including GPS mapping, sensors, and drones, allows sugarcane and sugar beet farmers to optimize water usage, fertilizers, and pest control. This leads to increased crop yields and higher sugar production. Biotechnology is leading to the development of genetically modified or hybrid sugarcane and sugar beet varieties that offer higher resistance to pests and diseases, as well as better adaptability to various climates. These advancements boost sugarcane productivity and ensure consistent supply. Mechanized sugarcane harvesting reduces labor costs and improves efficiency in countries where manual labor is traditionally used. It also allows for more precise and timely harvesting, minimizing crop waste and maximizing yields.

Request for a sample copy of this report: https://www.imarcgroup.com/sugar-manufacturing-plant/requestsample

Sugar Market Report Segmentation:

Breakup By Product Type:

- White Sugar

- Brown Sugar

- Liquid Sugar

White Sugar represents the largest segment because it is the most commonly used form of refined sugar in households, food processing, and beverages due to its purity and versatility.

Breakup By Form:

- Granulated Sugar

- Powdered Sugar

- Syrup Sugar

Granulated sugar accounts for the majority of the market share owing to its utilization in cooking, baking, and industrial food production due to its ease of handling, storage, and measurement.

Breakup By End-Use Sector:

- Food and Beverages

- Pharma and Personal Care

- Household

Food and beverages hold the biggest market share due to its key role in a wide range of processed foods, beverages, and confectionery products.

Breakup by Source:

- Sugarcane

- Sugar Beet

A detailed breakup and analysis of the sugar market based on the source has also been provided in the market report.

Breakup By Region:

- North America (United States, Canada)

- Asia Pacific (China, Japan, India, South Korea, Australia, Indonesia, Others)

- Europe (Germany, France, United Kingdom, Italy, Spain, Russia, Others)

- Latin America (Brazil, Mexico, Others)

- Middle East and Africa

Brazil enjoys the leading position in the sugar market as it is the largest producer and exporter of sugar globally, driven by its massive sugarcane industry and favorable climatic conditions.

Top Sugar Market Leaders:

The sugar market research report outlines a detailed analysis of the competitive landscape, offering in-depth profiles of major companies. Some of the key players in the market are:

- Absolute Aromas Ltd

- Albert Vieille (Givaudan SA)

- Aromatic Herbals Private Limited

- Berje Inc

- Edens Garden

- Ernesto Ventos S.A.

- StBotanica

- UniKode S.A.

- Van Aroma

- Vigon International LLC

If you require any specific information that is not covered currently within the scope of the report, we will provide the same as a part of the customization.

About Us:

IMARC Group is a global management consulting firm that helps the world’s most ambitious changemakers to create a lasting impact. The company provide a comprehensive suite of market entry and expansion services. IMARC offerings include thorough market assessment, feasibility studies, company incorporation assistance, factory setup support, regulatory approvals and licensing navigation, branding, marketing and sales strategies, competitive landscape and benchmarking analyses, pricing and cost research, and procurement research.

Contact Us:

IMARC Group

134 N 4th St. Brooklyn, NY 11249, USA

Email: sales@imarcgroup.com

Tel No:(D) +91 120 433 0800

United States: +1-631-791-1145 | United Kingdom: +44-753-713-2163