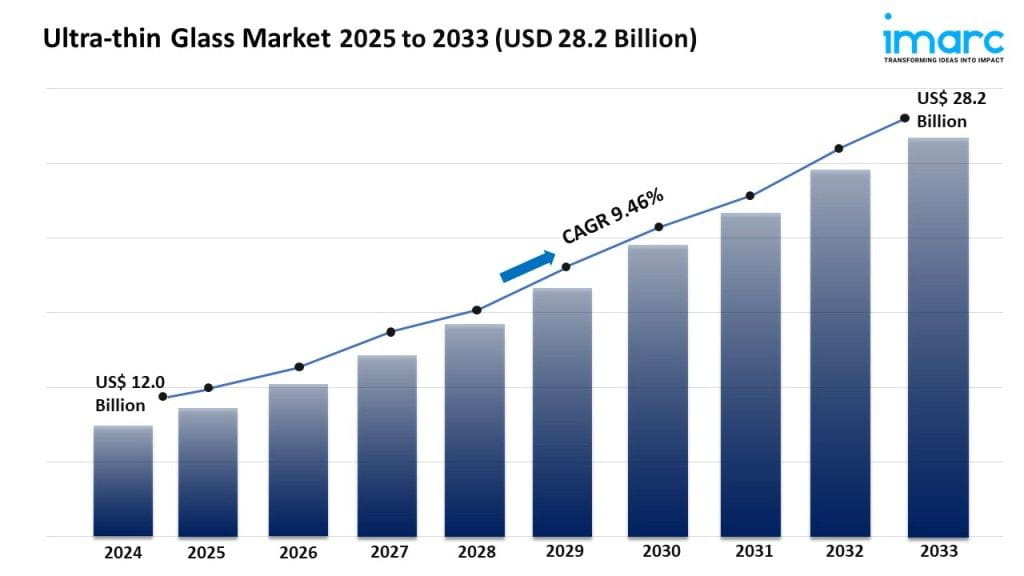

IMARC Group’s report titled “Ultra-thin Glass Market Report by Thickness Type (<0.1 Mm, 0.1 Mm-0.5 Mm, 0.5 Mm-1.0 Mm), Manufacturing Process (Float, Fusion, Down-Draw), Application (Semiconductor Substrate, Touch Panel Displays, Fingerprint Sensors, Automotive Glazing, and Others), End Use Industry (Consumer Electronics, Automotive, Biotechnology, and Others), and Region 2025-2033”. The global ultra-thin glass market size reached USD 12.0 Billion in 2024. Looking forward, IMARC Group expects the market to reach USD 28.2 Billion by 2033, exhibiting a growth rate (CAGR) of 9.46% during 2025-2033.

Grab a sample PDF of this report: https://www.imarcgroup.com/ultra-thin-glass-market/requestsample

Factors Affecting the Growth of the Ultra-Thin Glass Industry:

- Technological Advancements in Display Technology:

The continuous advancements in display technology are impelling the growth of the market. As electronic devices are evolving, there is an increase in the demand for thinner, lighter, and more flexible glass solutions. Ultra-thin glass is pivotal in the development of next-generation products, such as foldable and rollable displays, touch-sensitive surfaces, and high-resolution screens. This glass is essential for applications requiring high transparency, enhanced durability, and superior touch sensitivity, making it indispensable in smartphones, tablets, televisions (TVs), and wearable technology.

- Expansion in the Renewable Energy Sector:

The expansion of renewable energy, particularly solar energy, plays a crucial role in driving the demand for ultra-thin glass. This glass is a key component in photovoltaic modules and solar mirrors, where it is valued for its high light transmittance, low reflectance, and durability. Its ultra-thin nature ensures minimal light absorption, maximizing the efficiency of solar panels and contributing to more effective energy conversion. As the global push for sustainable energy solutions intensifies, the deployment of solar energy systems is rising. Governments worldwide are implementing policies and incentives to encourage the adoption of solar energy, which, in tur,n is driving the demand for high-quality, durable, and efficient materials like ultra-thin glass, essential for achieving long-term performance and reliability in solar installations.

- Growing Demand in the Automotive Industry:

Ultra-thin glass is increasingly becoming a material of choice in the automotive industry, driven by the shift towards more sophisticated and energy-efficient vehicles. It is being utilized in automotive displays, touch interfaces, and increasingly in windows and sunroofs, offering advantages, such as reduced weight, improved fuel efficiency, and enhanced aesthetic appeal. The integration of advanced driver-assistance systems (ADAS) and the progression towards autonomous vehicles are further amplifying the need for high-quality, durable ultra-thin glass. It provides critical solutions for heads-up displays, sensors, and cameras, ensuring clarity, durability, and high-performance under varying environmental conditions.

Leading Companies Operating in the Global Ultra-Thin Glass Industry:

- AGC Inc.

- Central Glass Co. Ltd.

- Changzhou Almaden Co. Ltd.

- Corning Incorporated

- CSG Holding Limited

- Emerge Glass India Pvt. Ltd.

- Fraunhofer FEP

- Nippon Electric Glass Co. Ltd.

- Nippon Sheet Glass Co. Ltd

- Noval Glass Goup Ltd.

- Schott AG (Carl-Zeiss-Stiftung)

- Taiwan Glass Industry Corporation

Ultra-Thin Glass Market Report Segmentation:

By Thickness Type:

- <0.1 Mm

- 0.1 Mm-0.5 Mm

- 0.5 Mm-1.0 Mm

0.1 mm-0.5 mm represents the largest segment as it offers enhanced flexibility and bendability.

By Manufacturing Process:

- Float

- Fusion

- Down-Draw

Float accounts for the majority of the market share due to its uniform thickness and flatness.

By Application:

- Semiconductor Substrate

- Touch Panel Displays

- Fingerprint Sensors

- Automotive Glazing

- Others

Touch panel displays hold the biggest market share owing to the rising demand for ultra-thin glass in the production of smartphones and other electronic devices with touch panels.

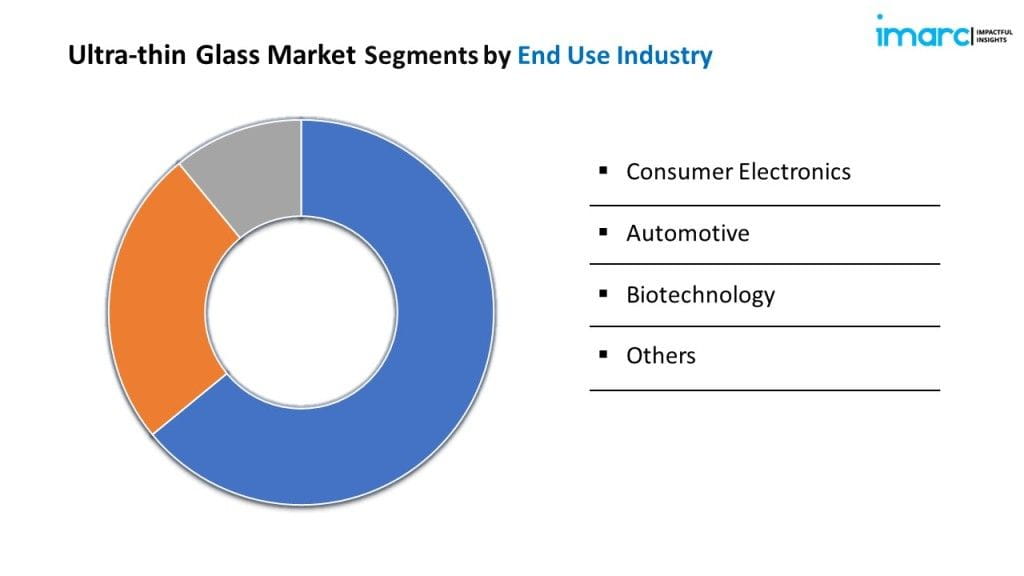

By End Use Industry:

- Consumer Electronics

- Automotive

- Biotechnology

- Others

Consumer electronics represents the leading segment driven by the rising demand for smart devices among the masses.

Regional Insights:

- North America (United States, Canada)

- Asia Pacific (China, Japan, India, South Korea, Australia, Indonesia, Others)

- Europe (Germany, France, United Kingdom, Italy, Spain, Russia, Others)

- Latin America (Brazil, Mexico, Others)

- Middle East and Africa

Asia Pacific’s dominance in the ultra-thin glass market is attributed to the increasing use of ultra-thin glass in the semiconductor industry.

Global Ultra-Thin Glass Market Trends:

The rising demand for ultra-thin glass, given its exceptional properties like chemical stability, barrier protection, and compatibility with sterilization processes, is bolstering the market growth. Ultra-thin glass is widely utilized in the packaging of sensitive pharmaceutical formulations, vials, syringes, and ampoules, where maintaining the purity and efficacy of the medication is paramount. Its non-reactive nature ensures that there is no interaction with the contents, thereby preserving the medicinal properties and extending the shelf life of pharmaceutical products. Additionally, the shift towards more sustainable packaging solutions and the stringent regulations governing pharmaceutical packaging are propelling the adoption of ultra-thin glass. Its superior durability and resistance to breakage also enhance the safety and integrity of pharmaceutical packaging, making it a preferred choice for high-quality, reliable, and safe packaging solutions in the healthcare industry.

Note: If you need specific information that is not currently within the scope of the report, we will provide it to you as a part of the customization.

About Us:

IMARC Group is a leading market research company that offers management strategy and market research worldwide. We partner with clients in all sectors and regions to identify their highest-value opportunities, address their most critical challenges, and transform their businesses.

IMARCs information products include major market, scientific, economic and technological developments for business leaders in pharmaceutical, industrial, and high technology organizations. Market forecasts and industry analysis for biotechnology, advanced materials, pharmaceuticals, food and beverage, travel and tourism, nanotechnology and novel processing methods are at the top of the company’s expertise.

Our offerings include comprehensive market intelligence in the form of research reports, production cost reports, feasibility studies, and consulting services. Our team, which includes experienced researchers and analysts from various industries, is dedicated to providing high-quality data and insights to our clientele, ranging from small and medium businesses to Fortune 1000 corporations.

Contact US:

IMARC Group

134 N 4th St. Brooklyn, NY 11249, USA

Email: sales@imarcgroup.com

Tel No:(D) +91 120 433 0800

United States: +1-631-791-1145