Global COPD and Asthma Devices Industry: Key Statistics and Insights in 2024-2032

Summary:

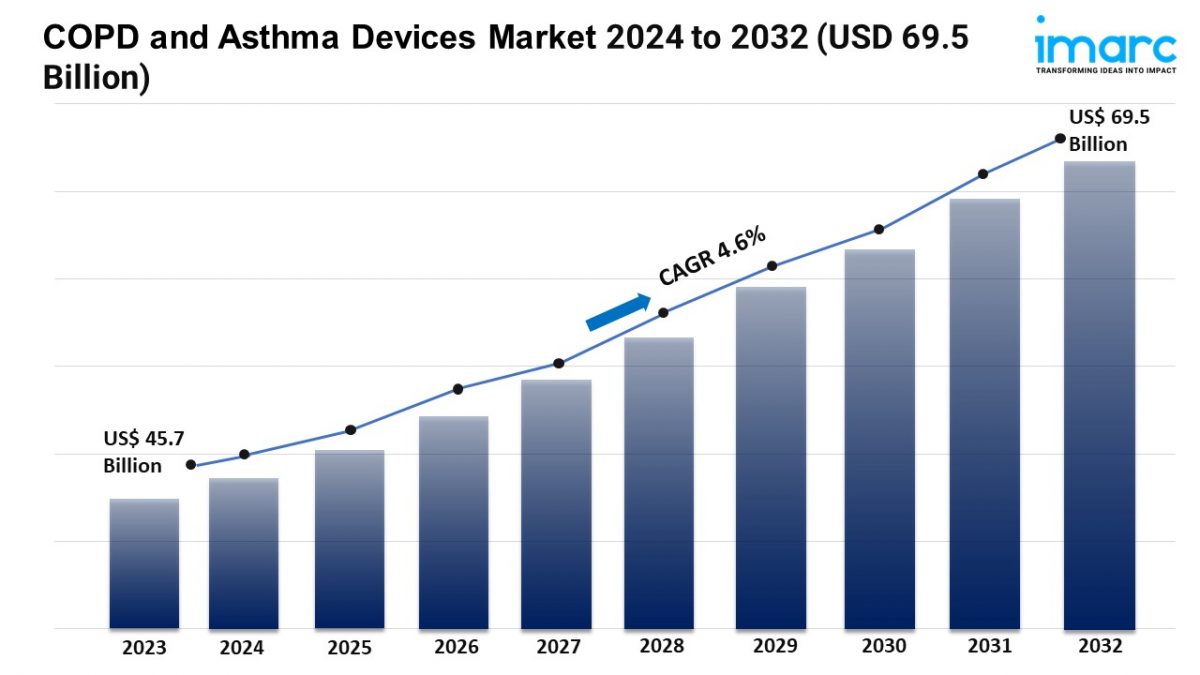

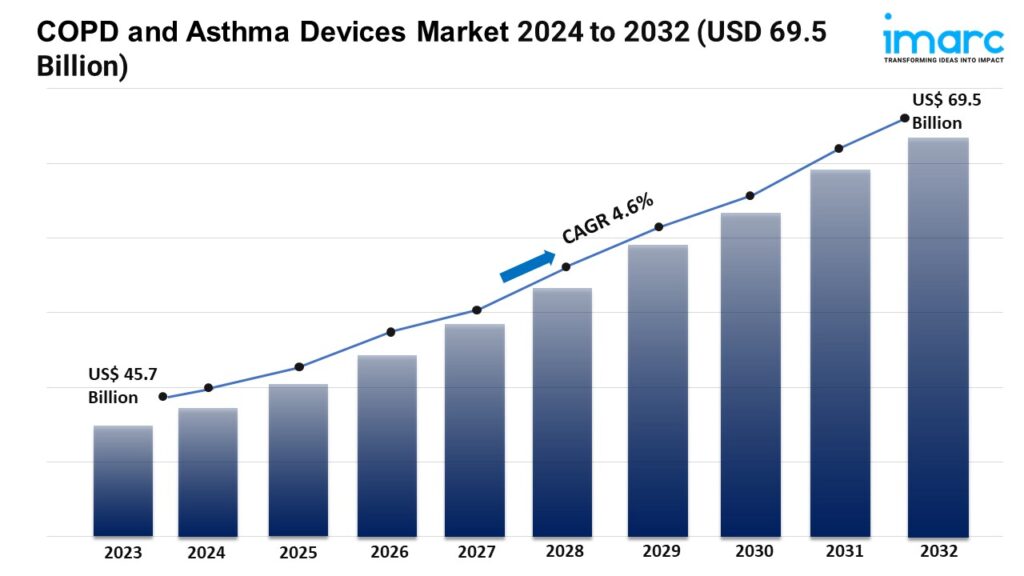

- The global COPD and asthma devices market size reached USD 45.7 Billion in 2023.

- The market is expected to reach USD 69.5 Billion by 2032, exhibiting a growth rate (CAGR) of 4.6% during 2024-2032.

- North America leads the market, accounting for the largest COPD and asthma devices market share.

- Asthma, driven by factors like air pollution and genetics, is the dominant segment in the inhaler market due to its higher prevalence.

- Retail pharmacies dominate the market for inhalers, offering patients convenient access to their prescribed devices.

- The increasing prevalence of respiratory diseases, caused by factors like air pollution, smoking, and lifestyle changes, is driving the demand for inhalers.

- Smart inhalers with features like Bluetooth technology and usage tracking are improving drug delivery efficiency and patient adherence.

- Older adults are at a higher risk of chronic respiratory diseases due to age-related lung decline, smoking, and exposure to air pollutants.

Industry Trends and Drivers:

- Increasing Prevalence of Respiratory Diseases:

The rising occurrence of respiratory diseases among the masses, attributed to a combination of factors, including air pollution, smoking, and changing lifestyle habits, is bolstering the market growth. Urbanization is leading to higher levels of air pollutants, such as particulate matter and nitrogen dioxide, which exacerbate respiratory conditions. Furthermore, the growing smoking population is contributing to the incidence of chronic obstructive pulmonary disease (COPD) and asthma. These factors are catalyzing the demand for effective and convenient respiratory devices, including inhalers and nebulizers, to manage and treat these conditions. Healthcare systems and patients are seeking more efficient treatment options, which is driving the need for COPD and asthma devices.

- Technological Advancements in Device Manufacturing:

Innovations in device design and functionality, such as the development of smart inhalers equipped with Bluetooth technology, offer enhanced drug delivery efficiency and patient adherence through features like usage tracking and reminders. Manufacturers are focusing on creating compact, user-friendly devices that improve the quality of life for patients with respiratory conditions. These advancements not only cater to the demand for more efficient treatment options but also support the shift towards personalized medicine. The continuous technological evolution is leading to the adoption of advanced COPD and asthma devices with enhanced features.

- Rise in Geriatric Population:

Older adults are more susceptible to chronic respiratory diseases due to the natural decline in lung function with age, compounded by factors, such as a history of smoking and increased vulnerability to air pollutants. This demographic shift is leading to a higher incidence of COPD and asthma, thereby catalyzing the demand for respiratory care devices. The need for easy-to-use and effective treatment options for older people is encouraging innovation and adoption of devices specifically designed to cater to this age group. The growing aging population is driving the demand for COPD and asthma devices.

Grab a sample PDF of this report: https://www.imarcgroup.com/copd-asthma-devices-market/requestsample

COPD and Asthma Devices Market Report Segmentation:

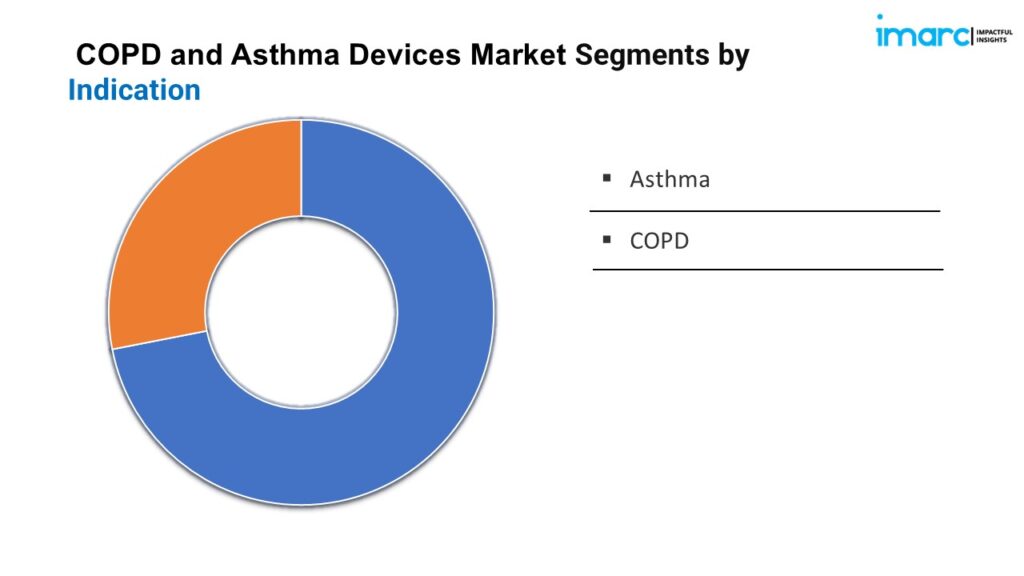

By Indication:

- Asthma

- COPD

Asthma represents the largest segment owing to its higher prevalence among the masses through factors, such as air pollution and genetic predisposition.

By Distribution Channel:

- Retail Pharmacies

- Hospitals

- Online Pharmacies

Retail pharmacies hold the biggest market share, as they are the most accessible source for patients to obtain their prescribed devices.

Regional Insights:

- North America (United States, Canada)

- Asia Pacific (China, Japan, India, South Korea, Australia, Indonesia, Others)

- Europe (Germany, France, United Kingdom, Italy, Spain, Russia, Others)

- Latin America (Brazil, Mexico, Others)

- Middle East and Africa

North America dominates the market owing to the presence of an advanced healthcare infrastructure and the rising prevalence of respiratory conditions within its population.

Top COPD and Asthma Devices Market Leaders:

The COPD and asthma devices market research report outlines a detailed analysis of the competitive landscape, offering in-depth profiles of major companies. Some of the key players in the market are:

- Adherium Limited

- Aristopharma Ltd.

- AstraZeneca PLC

- Baxter International Inc.

- Boehringer Ingelheim International GmbH

- Cohero Health Inc.

- Koninklijke Philips N.V.

- Omron Corporation

- Pari Respiratory Equipment Inc.

- Recipharm AB

- Verona Pharma plc

If you require any specific information that is not covered currently within the scope of the report, we will provide the same as a part of the customization.

About Us:

IMARC Group is a global management consulting firm that helps the world’s most ambitious changemakers to create a lasting impact. The company provide a comprehensive suite of market entry and expansion services. IMARC offerings include thorough market assessment, feasibility studies, company incorporation assistance, factory setup support, regulatory approvals and licensing navigation, branding, marketing and sales strategies, competitive landscape and benchmarking analyses, pricing and cost research, and procurement research.

Contact Us:

IMARC Group

134 N 4th St. Brooklyn, NY 11249, USA

Email: sales@imarcgroup.com

Tel No:(D) +91 120 433 0800

United States: +1-631-791-1145