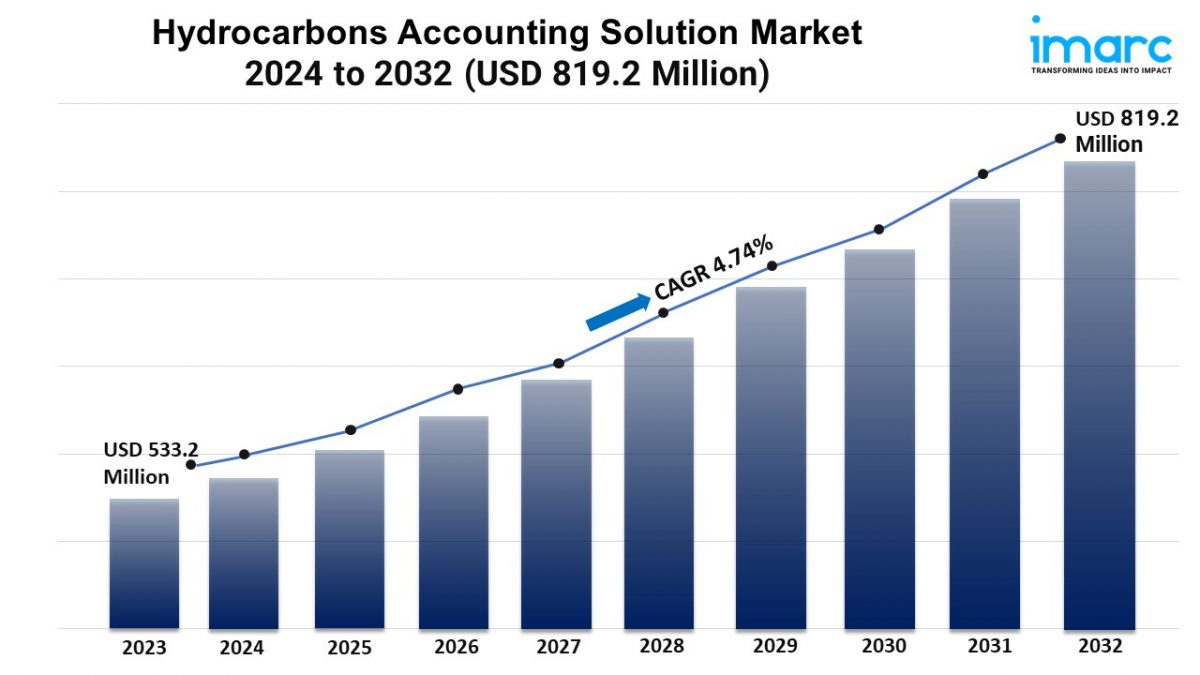

IMARC Group’s report titled “Hydrocarbons Accounting Solution Market Report by Component (Software, Services), Deployment Mode (On-premises, Cloud-based), Application (Oil, Natural Gas, Water), End User (Upstream Companies, Mid-Stream Companies, Downstream Companies), and Region 2024-2032″, The global hydrocarbons accounting solution market size reached US$ 533.2 Million in 2023. Looking forward, IMARC Group expects the market to reach US$ 819.2 Million by 2032, exhibiting a growth rate (CAGR) of 4.74% during 2024-2032.

For an in-depth analysis, you can refer sample copy of the report: https://www.imarcgroup.com/hydrocarbons-accounting-solution-market/requestsample

Factors Affecting the Growth of the Hydrocarbons Accounting Solution Industry:

- Regulatory Compliance:

Governing agencies of various countries are implementing several standards mandating accurate tracking and reporting of hydrocarbon production, sales, and distribution. Hydrocarbons accounting solutions ensure adherence to these requirements by providing robust data management, audit trails, and reporting capabilities. Compliance with regulations, such as emissions reporting, royalties, and taxation, is critical for avoiding penalties, maintaining licenses, and safeguarding the reputation of the company. These solutions also offer flexibility to adapt to evolving regulatory frameworks and enable companies to stay ahead of compliance challenges and mitigate regulatory risks effectively.

- Operational Efficiency:

In the oil and gas industry, operational efficiency is paramount for maximizing profits and staying ahead of the competition. Hydrocarbons accounting solutions streamline various processes involved in production monitoring, inventory management, and revenue reconciliation, leading to efficiency gains. These solutions enable companies to optimize resource utilization, minimize downtime, and improve overall productivity by automating repetitive tasks, reducing manual errors, and providing real-time insights into operations. Enhanced operational efficiency translates to cost savings, increased output, and better decision-making, empowering oil and gas companies to achieve their production targets.

- Increasing Complexity:

The oil and gas industry is increasingly becoming complex with the exploration of unconventional reserves and the development of integrated energy projects. Hydrocarbons accounting solutions play a crucial role in managing this complexity by providing advanced capabilities to handle diverse data sources, complex calculations, and integration with other enterprise systems. These solutions offer scalability, flexibility, and customization options to adapt to the evolving needs of oil and gas companies operating in diverse environments. Hydrocarbons accounting solutions simplify complex workflows, improve data accuracy, and enhance decision-making capabilities by centralizing and standardizing accounting processes across the organization.

Leading Companies Operating in the Global Hydrocarbons Accounting Solution Industry:

- CGI Inc.

- EnergySys Limited

- Infosys Limited

- P2 Energy Solutions

- Quorum Business Solutions Inc.

- SAP SE

- Wipro Limited

Hydrocarbons Accounting Solution Market Report Segmentation:

By Component:

- Software

- Services

- Consulting

- Implementation

- Support

Software represents the largest segment as it is designed to handle complex tasks, such as tracking hydrocarbon production, consumption, and losses.

By Deployment Mode:

- On-premises

- Cloud-based

Cloud-based holds the biggest market share on account of its enhanced scalability, flexibility, and cost-efficiency.

By Application:

- Oil

- Natural Gas

- Water

Oil accounts for the largest market share due to the increasing focus on tracking and managing oil resources.

By End User:

- Upstream Companies

- Mid-Stream Companies

- Downstream Companies

Upstream companies exhibit a clear dominance in the market, driven by the rising need to maximize resource recovery while minimizing costs and environmental impact.

Regional Insights:

- North America (United States, Canada)

- Asia Pacific (China, Japan, India, South Korea, Australia, Indonesia, Others)

- Europe (Germany, France, United Kingdom, Italy, Spain, Russia, Others)

- Latin America (Brazil, Mexico, Others)

- Middle East and Africa

North America enjoys a leading position in the hydrocarbons accounting solution market, which can be attributed to the thriving oil and gas sector.

Global Hydrocarbons Accounting Solution Market Trends:

The rising adoption of advanced technologies, such as the Internet of Things (IoT), artificial intelligence (AI), and analytics in the oil and gas sector is bolstering the market growth. Hydrocarbons accounting solutions provide the data infrastructure and analytical capabilities required to unlock actionable insights from operational data. These solutions enable companies to optimize production processes, reduce costs, and identify new revenue opportunities by leveraging real-time data analytics, predictive modeling, and ML algorithms. Furthermore, they facilitate collaboration and knowledge sharing across the organization, which is impelling the market growth.

Moreover, oil and gas companies are increasingly focused on optimizing the performance of their assets to maximize returns.

Note: If you need specific information that is not currently within the scope of the report, we will provide it to you as a part of the customization.

About Us:

IMARC Group is a leading market research company that offers management strategy and market research worldwide. We partner with clients in all sectors and regions to identify their highest-value opportunities, address their most critical challenges, and transform their businesses.

IMARCs information products include major market, scientific, economic and technological developments for business leaders in pharmaceutical, industrial, and high technology organizations. Market forecasts and industry analysis for biotechnology, advanced materials, pharmaceuticals, food and beverage, travel and tourism, nanotechnology and novel processing methods are at the top of the companys expertise.

Our offerings include comprehensive market intelligence in the form of research reports, production cost reports, feasibility studies, and consulting services. Our team, which includes experienced researchers and analysts from various industries, is dedicated to providing high-quality data and insights to our clientele, ranging from small and medium businesses to Fortune 1000 corporations.

Contact Us:

IMARC Group

134 N 4th St. Brooklyn, NY 11249, USA

Email: sales@imarcgroup.com

Tel No:(D) +91 120 433 0800

United States: +1-631-791-1145 | United Kingdom: +44-753-713-2163