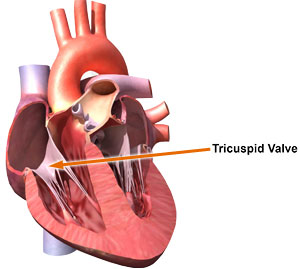

The Tricuspid Valve Repair Market, growing due to increased tricuspid valve diseases and surgical advancements, reached $622.94 million in 2023 with a 7.4% CAGR and is projected to hit $973.5 million by 2032, signaling ongoing expansion and industry opportunities.The tricuspid valve, often overlooked compared to its counterparts, plays a crucial role in cardiac function. Its dysfunction can lead to significant health complications, necessitating surgical intervention. In recent years, the tricuspid valve repair market has witnessed notable advancements driven by technological innovation and a growing understanding of valvular disorders. This article delves into the trends and innovations shaping this market.

Browse the full report at https://www.credenceresearch.com/report/tricuspid-valve-repair-market

Growing Prevalence and Awareness:

The prevalence of tricuspid valve disorders, particularly tricuspid regurgitation (TR), is on the rise globally. Factors such as an aging population, increased incidence of heart diseases, and improved diagnostic techniques contribute to the growing awareness and diagnosis of tricuspid valve dysfunction. As a result, there is a heightened demand for effective treatment options, propelling growth in the tricuspid valve repair market.

Minimally Invasive Procedures:

Traditionally, tricuspid valve repair involved open-heart surgery, which carried significant risks and prolonged recovery times. However, advancements in minimally invasive techniques have revolutionized the treatment landscape. Procedures such as transcatheter tricuspid valve repair offer a less invasive alternative, reducing morbidity and mortality rates while enhancing patient outcomes. The adoption of these techniques continues to grow, driving market expansion.

Technological Advancements:

Technological innovations have played a pivotal role in refining tricuspid valve repair procedures. From advanced imaging modalities for precise diagnosis to novel devices for repair and replacement, technology continues to push the boundaries of what is possible in cardiac care. For instance, 3D printing allows for the creation of patient-specific models, enabling surgeons to plan and practice complex procedures with greater accuracy. Similarly, the development of biocompatible materials and tissue-engineered constructs holds promise for durable and biologically compatible valve repairs.

Focus on Functional Tricuspid Regurgitation:

While organic tricuspid valve disease is a primary concern, functional tricuspid regurgitation (FTR) represents a significant proportion of cases. FTR often accompanies left-sided heart disease and is associated with poor outcomes if left untreated. Recognizing the impact of FTR on patient prognosis, there is a growing emphasis on addressing this condition through targeted interventions. Innovative approaches such as annuloplasty devices and chordal implantation techniques aim to restore valve function and improve patient quality of life.

Collaborative Research and Clinical Trials:

Collaboration between industry stakeholders, healthcare providers, and research institutions drives progress in the tricuspid valve repair market. Clinical trials play a vital role in evaluating the safety and efficacy of new interventions, facilitating evidence-based decision-making. With an increasing number of companies investing in research and development, the pipeline for novel tricuspid valve repair technologies remains robust. These collaborative efforts accelerate innovation and pave the way for the introduction of transformative therapies.

Challenges and Opportunities:

Despite the advancements, challenges persist in the tricuspid valve repair market. Access to advanced procedures may be limited in certain regions, exacerbating healthcare disparities. Additionally, the complexity of tricuspid valve anatomy and pathology presents technical challenges for clinicians. However, these challenges also present opportunities for innovation and collaboration. By addressing unmet clinical needs and leveraging emerging technologies, the market can overcome barriers and improve patient outcomes.

Key Players

- Edwards Lifesciences Corporation

- Abbott Laboratories

- Medtronic plc

- Boston Scientific Corporation

- LivaNova PLC

- Micro Interventional Devices, Inc.

- Neovasc Inc.

- MVRx, Inc.

- Millipede, Inc.

- Harpoon Medical, Inc.

Segmentations

By End User

- Hospitals

- Ambulatory Surgical Centers

- Specialty Clinics

By Indication

- Tricuspid Regurgitation

- Tricuspid Stenosis

- Other Tricuspid Valve Disorders

By Distribution Channel

- Direct Sales

- Distributors

- Online Platforms

By Region

- North America

- The U.S.

- Canada

- Mexico

- Europe

- Germany

- France

- The U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of Middle East and Africa

About Us:

Credence Research is committed to employee well-being and productivity. Following the COVID-19 pandemic, we have implemented a permanent work-from-home policy for all employees.

Contact:

Credence Research

Please contact us at +91 6232 49 3207

Email: sales@credenceresearch.com