Summary:

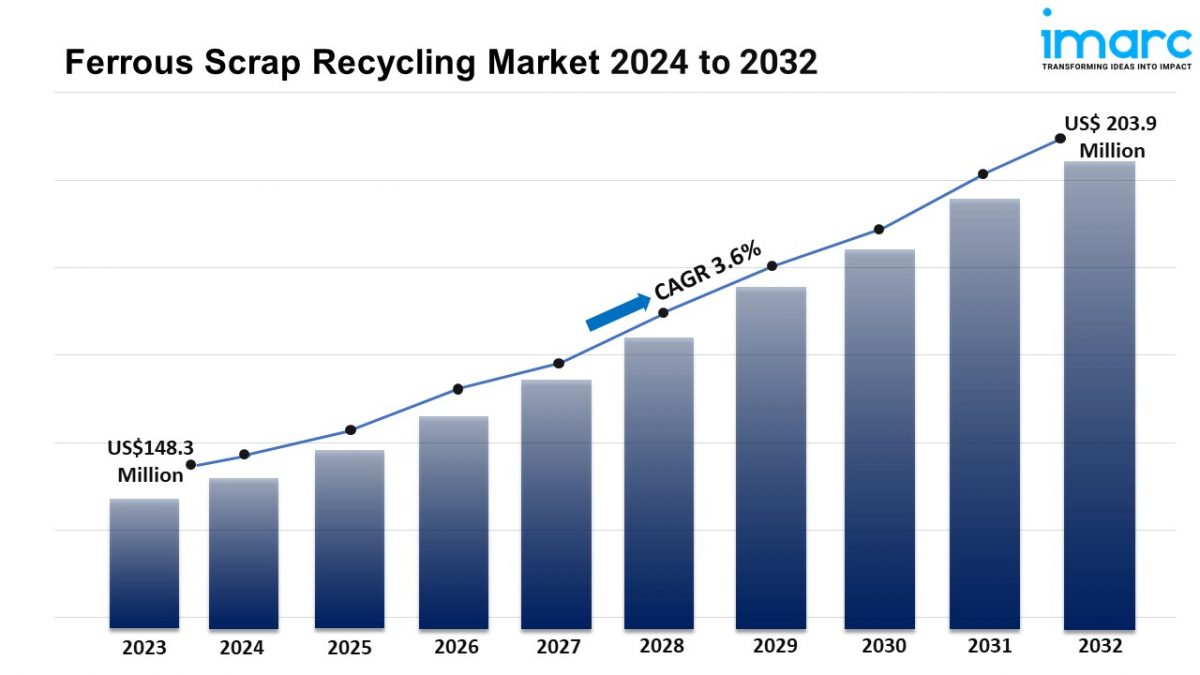

- The global ferrous scrap recycling market size reached USD 148.3 Million in 2023.

- The market is expected to reach USD 203.9 Million by 2032, exhibiting a growth rate (CAGR) of 3.6% during 2024-2032.

- Europe leads the market, accounting for the largest ferrous scrap recycling market share.

- Old car bodies accounts for the majority of the market share in the type segment due to their simplicity, functionality, and aesthetic appeal.

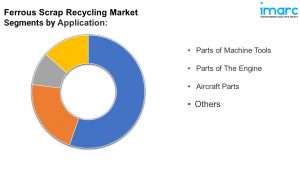

- Based on the application, the market has been segmented into parts of machine tools, parts of the engine, aircraft parts, and others.

- Construction remains a dominant segment in the market as it requires substantial amounts of recycled steel for building and infrastructure developments.

- The growing demand for sustainable manufacturing practices is a primary driver of the ferrous scrap recycling market.

- The advancement in recycling technologies is propelling the ferrous scrap recycling market.

Industry Trends and Drivers:

- Increasing Demand for Sustainable Practices in Manufacturing:

The push for sustainability across various industries is a significant driver in the growth of the ferrous scrap recycling market. Manufacturers are increasingly adopting recycled materials to reduce their carbon footprint, conserve natural resources, and meet stringent environmental regulations. Recycling ferrous scrap helps lower greenhouse gas emissions and reduces energy consumption in steel production compared to using virgin raw materials. As companies move toward more environmentally friendly production processes, the demand for recycled steel is rising. Additionally, governments and international organizations are implementing policies that encourage or mandate the use of recycled materials, further bolstering this trend. The construction and automotive industries, in particular, are major consumers of recycled ferrous scrap, as they look to incorporate more sustainable materials in their operations. This focus on sustainability is expected to continue driving growth in the ferrous scrap recycling market in the coming years.

- Technological Advancements in Recycling Processes:

Technological advancements are playing a crucial role in improving the efficiency and effectiveness of ferrous scrap recycling processes. Innovations in sorting technologies, such as magnetic separation and advanced shredders, are enabling recyclers to recover higher volumes of ferrous scrap with greater precision. These technologies are also reducing contamination, ensuring that the recycled materials meet industry standards for purity and quality. Automated systems for sorting and processing scrap metal are speeding up the recycling process while lowering labor costs, making recycling operations more profitable. Furthermore, advancements in data analytics and AI-driven technologies are helping recycling facilities optimize their operations by predicting scrap availability, managing inventory, and enhancing overall efficiency. As these technological innovations continue to evolve, they are expected to further enhance the ferrous scrap recycling market by reducing costs and improving the quality of recycled materials.

- Growing Global Steel Demand Boosting Scrap Utilization:

The rising global demand for steel is another significant trend driving the ferrous scrap recycling market. As construction, infrastructure development, and automotive production continue to grow, so does the need for steel, much of which can be sourced from recycled ferrous scrap. Emerging economies in regions like Asia-Pacific, Latin America, and Africa are experiencing rapid urbanization and industrialization, fueling a substantial increase in steel consumption. Recycled ferrous scrap plays a vital role in meeting this demand, offering a cost-effective and environmentally friendly alternative to producing steel from raw materials. Moreover, as countries strive to reduce reliance on raw material imports, the use of recycled scrap in domestic steel production is gaining traction. This trend is expected to contribute to the expansion of the global ferrous scrap recycling market, as steel producers seek to balance economic efficiency with environmental sustainability.

Request Sample For PDF Report: https://www.imarcgroup.com/ferrous-scrap-recycling-market/requestsample

Report Segmentation:

The report has segmented the market into the following categories:

Breakup by Type:

- Heavy Melting Steel

- Old Car Bodies

- Cast Iron

- Pressing Steel

- Others

Old car bodies account for the majority of shares as they provide a significant source of recyclable ferrous scrap due to the high metal content in vehicles.

Breakup by Application:

- Parts of Machine Tools

- Parts of The Engine

- Aircraft Parts

- Others

Based on the application, the market has been segmented into parts of machine tools, parts of the engine, aircraft parts, and others.

Breakup by End User:

- Construction

- Automotive

- Shipbuilding

- Equipment Manufacturing

- Consumer Appliances

- Others

Construction represents the majority of shares as it utilizes large quantities of recycled steel for infrastructure and building projects.

Market Breakup by Region:

- North America (United States, Canada)

- Asia Pacific (China, Japan, India, South Korea, Australia, Indonesia, Others)

- Europe (Germany, France, United Kingdom, Italy, Spain, Russia, Others)

- Latin America (Brazil, Mexico, Others)

- Middle East and Africa

Europe holds the leading position owing to strict environmental regulations and a strong emphasis on recycling and sustainability initiatives across the region.

Top Ferrous Scrap Recycling Market Leaders:

- American Iron & Metal Co Inc

- European Metal Recycling Ltd.

- OmniSource, LLC (Steel Dynamics, Inc.)

- Schnitzer Steel Industries, Inc.

- Sims Limited

- TSR Recycling GmbH & Co. KG (Remondis SE & Co. KG)

- Ward Recycling Limited

If you need specific information that is not currently within the scope of the report, we will provide it to you as a part of the customization.

About Us

IMARC Group is a global management consulting firm that helps the world’s most ambitious changemakers to create a lasting impact. The company provide a comprehensive suite of market entry and expansion services. IMARC offerings include thorough market assessment, feasibility studies, company incorporation assistance, factory setup support, regulatory approvals and licensing navigation, branding, marketing and sales strategies, competitive landscape and benchmarking analyses, pricing and cost research, and procurement research.